High Demand Drives 3PLs to Best Growth Year on Record

[Stay on top of transportation news: Get TTNews in your inbox.]

Strong consumer demand, continued supply chain bottlenecks and tight carrier capacity sent air, ground and ocean transportation rates soaring to historic levels in 2021 as shippers leaned on third-party logistics providers to bolster inventories and avoid product stockouts.

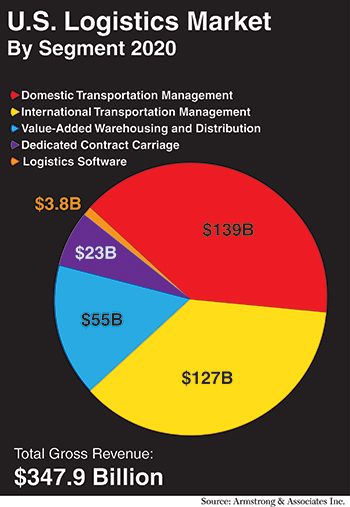

Even as many 3PLs still are providing us with 2021 financial results, Armstrong & Associates’ current estimates show the U.S. 3PL market gross revenues grew a whopping 50.3%, bringing the total U.S. 3PL market to $347.9 billion.

Year-over-year, 2021 saw the fastest 3PL growth since we began estimating the market size in 1995, but 3PL market segment growth was uneven. While the dedicated contract carriage (DCC) and value-added warehousing and distribution (VAWD) segments had a great year with 15.3% and 17.8% gross revenue growth respectively, most of the overall growth came from international transportation management (ITM) with 81.4% year-over-year growth and domestic transportation management (DTM) with 52.4% growth.

Armstrong

To meet demand, 3PLs in ITM and DTM increasingly tapped the spot market to source carriers to cover shipments. While strong demand drove growth across the 3PL market, the true leaders were 3PLs with strong carrier management skills that have technologically innovated, allowing them to efficiently tap long-standing carrier relationships to cover shipper demand versus being overreliant on using load boards or traditional means to buy capacity at spot market rates.

Total 3PL segment net revenues (gross revenues minus purchased transportation) grew 28.1% to $119.7 billion, reflecting gross margin compression due to a volatile carrier sourcing market and transportation management 3PLs spending more to secure hard-to-find carrier capacity. The overall gross margin for all segments declined from 40% to 34%.

Strong international and domestic transportation demand continued into 2022, providing support to lofty domestic and international transportation rates. With inventories increasing, COVID-19 case counts waning, and Federal Reserve rate hikes trying to curb inflation potentially slowing the economy, demand for domestic U.S. DTM and DCC 3PL services has become more stable and manageable.

►3PLs Get Chance to Prove Their Worth

►Clevenger: Why the List Expanded

►Map: Where the Top 100 Are

►Armstrong: Best Growth Year Ever

►Expansion Tweaks Sector Rankings

►Impact of Entrepreneurial Carriers

►Don't Make Same TMS Mistake Twice

Sector Rankings

Freight Brokerage | Dedicated

Dry Storage Warehousing

Refrigerated Warehousing

Ocean Freight | Airfreight

We anticipate domestic transportation rates will continue normalizing into the second half of the year, with the main caveat being the cost of fuel, which has been driven up by strong demand and oil and gas supply constraints due to Russia’s war in Ukraine. This dynamic should drive overall declines in base truckload rates, but with heavy fuel surcharges while the cost of oil remains high. Additionally, the driver shortage remains a headwind, and domestic transportation demand can drop further and faster if the Federal Reserve overdoes interest rate hikes to stave off inflation and drives the economy into recession in 2023.

The ITM environment this year has seen increased willingness for ocean carriers to provide contracted capacity and good rates for targeted port-to-port pairs, but with fewer fee waivers and increased surcharges. On the airfreight side, carriers remain constrained without passenger capacity and are not as amenable to contract for space. Even large airfreight forwarders still are sourcing 30% or more of their air capacity in the spot market.

Continued COVID shutdowns in Asia, disrupted sailing schedules, ocean port congestion and equipment issues, limited passenger air capacity, the cost of fuel and a potential longshoreman work stoppage in California will keep international supply chains in limbo and rates high well into next year.

VAWD will continue to do well given the general lack of warehousing space, which is nearing a critical level in the cold chain, and strong growth in e-commerce fulfillment and last-mile delivery. A lot of shippers we work with are examining their supply chain networks and providers to improve inventory management and on-time delivery performance. We anticipate continued focus on supply chain network flexibility and warehouse optimization.

International Transportation Management

Recapping 2021, international transportation management, which consists of air and ocean freight forwarding, customs brokerage and complementary value-added services, led all 3PL segments with revenue growth.

Overall, ITM realized an unheard-of 81.4% gross revenue gain in 2021, increasing to $127 billion, while underlying global ocean carrier container rates more than doubled from 2020 and airfreight rates trended up, peaking in December. While having a lower growth rate than overall gross revenue due to a tight carrier capacity market and high spot market rates, net revenue increased a healthy 46.2% to $36 billion.

C.H. Robinson’s Global Forwarding division more than doubled in 2021 with gross revenue growth of 117.1% to $6.7 billion. Net revenue increased 70.7% to $1.1 billion. C.H. Robinson now is a top freight forwarder in the Asia-to-U.S. trade lane. With 1.5 million in total ocean export TEUs (20-foot equivalent units) managed, it has surpassed longtime U.S.-headquartered competitor Expeditors International.

C.H. Robinson has grown rapidly via organic growth and acquisitions since 2011, when it had net revenue of $100 million. In 2012, it gained significant capabilities and scale via its $807 million acquisition of Phoenix International. From there, it added $251 million Australian provider APC Logistics in 2016, $124 million Canadian ITM Milgram in 2017 and $84 million Madrid-based Space Cargo in 2019.

Expeditors International is the largest U.S.-based ITM 3PL revenue-wise. Its 2021 gross revenue increased 67.7% to $16.5 billion, and net revenue grew 39.7% to $4.5 billion. Growth primarily came from ocean freight, in which gross revenue grew 137% to $5.5 billion from $2.3 billion in 2020. Expeditors’ ocean freight consolidation business grew 194%, primarily on exports from Asia. Airfreight gross revenue was up 58% to $6.8 billion. Net revenue grew at a lesser rate due to increased costs of purchased transportation in air and ocean, driving down overall gross profit margin to 27% from 32.4% in 2021.

In August, Denmark-headquartered DSV acquired Agility Integrated Global Logistics for $4.2 billion. With this acquisition, its 2019 acquisition of Panalpina and its 2016 acquisition of UTi Worldwide, DSV has grown to be the fourth-largest ocean freight forwarder globally with 2.9 million TEUs and the third-largest airfreight forwarder with 1.6 million metric tons. Last year, its Americas division grew year-over-year gross revenue 88.2% to $6 billion and net revenue by 48.3% to $1.1 billion with solid increases in both air and ocean volumes and revenues.

In late February 2021, Kuehne + Nagel announced it was buying Apex Logistics International for approximately $1.5 billion. The combination made Kuehne + Nagel the largest global airfreight forwarder, handling over 2.2 million metric air tons in 2021 and surpassing DHL Supply Chain & Global Forwarding. Apex also helped Kuehne + Nagel expand its Asian 3PL operating network, and its air charter operations added significantly to K+N’s net revenue in 2021. K+N’s Americas gross revenue grew 107.2% year-over-year to $8.7 billion and net revenue increased 141.6% to $1.9 billion.

Domestic Transportation Management

Non-asset-based domestic transportation management (DTM) includes freight brokerage, which is 83% of segment revenues, and managed transportation, which accounts for 17%. Like its ITM brethren, DTM 3PLs scrambled to find carrier capacity to meet shipper demand in 2021. Year-over-year gross revenue increased 52.4% to $139 billion, and net revenue increased 50.2% to $19.8 billion as strong demand and volatility in motor carrier capacity quickly increased spot market rates, compressing segment gross margins to 14.2% from 16.1% in pre-pandemic 2019.

The ongoing digitalization of transactional truckload DTM/freight brokerage continues at a rapid pace as more 3PLs have built API (application program interface) integrations into large shippers’ transportation management systems (TMS) for truckload spot-market rate quoting and automated load tendering and booking. A couple dozen 3PLs are using these TMS interfaces to provide shippers with instant spot rate quotes and the ability to complete load tendering and booking through the system APIs. This process automates traditional spot market freight brokerage sales functions and is increasing shippers’ use of more spot versus contract pricing.

Sales automation of spot market truckloads is happening in conjunction with the automation of carrier sales (procurement) functions within freight brokers using intelligent capacity management systems to digitally match shippers’ loads to carriers based upon historical and real-time carrier capacity data analyzed via machine learning/artificial intelligence algorithms. This digital freight matching (DFM) capability has become a competitive differentiator within the DTM segment as DTM 3PLs look to increase the number of loads/shipments they manage per person per day and revenue per person per year. It also can be vital to build carrier loyalty by reutilizing core carriers at rates that are below the spot market rates offered via load boards. Ultimately, DFM automation will put further pressure on freight brokerage gross margins as operating costs come down but should improve overall profitability through increased operational efficiency.

Arrive has grown rapidly since generating $31 million in sales during its first year of business. (Arrive Logistics)

The top five freight brokers — C.H. Robinson, Total Quality Logistics, Coyote Logistics, Echo Global Logistics and MODE Global — are some 3PLs driving industry automation, along with newer, tech-first digital freight brokers Convoy, Transfix and Uber Freight. At this point, most of the top freight brokers are strategically digitalizing operations to add value through improved carrier management and customer and carrier experiences.

The DTM “watch list” this year includes many 3PLs that “hit it out of the park” last year and leapfrogged over many long-standing competitors.

Arrive Logistics, founded by Matt Pyatt and other ex-Command Transportation staff in 2014, moved into 13th place, doubling gross revenue to $1.6 billion and generating estimated net revenue of $200 million from offices in Chicago and Austin, Texas. The company also has plans to open offices this year in San Antonio and Tampa, Fla. Arrive has grown rapidly since generating $31 million in sales during its first year of business. To help fuel growth, Arrive received a $300 million Series D private equity investment from ATL Partners in 2021. In 2022, Arrive acquired Forager Group’s cross-border business and proprietary systems platform from Matt Silver and team.

ArcBest Corp. was founded in 1923 in Fort Smith, Ark., and is the parent corporation of less-than-truckload industry stalwart ABF Freight. Its freight brokerage operations grew gross revenue 167% to $1.6 billion, moving it into 14th place on the list. Its net revenue climbed 132% to $195 million yielding it a gross margin of 12.3%. Acquisitions to expand the DTM operations of ArcBest include its November 2021 acquisition of Chicago-based truckload freight brokerage MoLo Solutions, along with its acquisitions of Logistics & Distribution Services Corp. in 2016 and Smart Lines Transportation Group and Bear Transportation Services in 2015.

Axle Logistics gets the “Who’s That?” award with a stellar gross revenue increase of 194% for $520 million in top-line revenue, driving it to 38th on the list. Axle was one of very few 3PLs with 2021 net revenue that grew faster than its gross revenue. With a 195.1% increase, Axle’s net revenue grew to $66.7 million. The company was founded in 2012 by University of Tennessee graduates Jon Clay and Drew Johnson. Based in Knoxville, Tenn., it has a staff of 260 managing dry van, flatbed, specialized truckloads and LTL and intermodal shipments within North America.

Value-Added Warehousing and Distribution

The value-added warehousing and distribution (VAWD) 3PL segment did well in 2021. Gross revenue increased 17.8% to $55 billion, and net revenue expanded 14.9% to $41 billion. Most VAWD 3PLs have full warehouses and have participated to some extent in the rapid growth of e-commerce fulfillment, which continues to be one of the fastest-growing domestic 3PL subsegments with annual growth of 24% from 2017 to 2021.

Many VAWD 3PLs are supporting retail brands’ strategies to manage their own order fulfillment channels and avoid being captive to large e-retailer platforms such as Amazon. Operationally, the growth in e-commerce business has meant an expansion in multiclient warehousing/fulfillment operations, many having footprints of less than 100,000 square feet.

An ongoing headwind for VAWD 3PLs has been the “Amazon effect.” 3PLs are continuing to see increased competition from Fulfillment by Amazon, which controls 60% of the U.S. e-commerce 3PL market. It has dramatically impacted warehouse employee wages and lease rates in key distribution areas such as Plainfield, Ind., and California’s Inland Empire. In turn, it is driving significant interest from VAWD 3PLs to automate warehouses with autonomous robotic solutions. With some autonomous robots costing less than $500 per month to operate, the cost-benefit and positive return on investment are increasing 3PLs’ interest in warehouse robots to support activities such as picking, put-away and cycle counting.

In terms of total dry warehousing square footage, DHL Supply Chain leads with 139 million square feet, followed by GXO Logistics with 90 million square feet, Ryder Supply Chain Solutions with 80 million, NFI with 60 million and Geodis North America with 52 million to round out the top five.

Americold provides extensive refrigerated and frozen warehousing. (Americold Logistics)

Cold chain leaders Americold and Lineage Logistics, which have been active acquirers, now command more than 50 million square feet of cold reefer/frozen storage space apiece.

In a tight cold chain warehouse capacity market, Americold North America increased net revenue 23.1% to $1.6 billion from 2020. With a network of 250 warehouses, Americold provides extensive refrigerated and frozen warehousing with value-added services for food products. Its customer list is a “Who’s Who” of the food business.

In January 2018, parent company Americold Realty Trust launched an initial public offering and now is listed on the New York Stock Exchange under ticker symbol COLD. Proceeds from the IPO paid off debt and funded new e-commerce services and acquisitions.

Two midmarket VAWD 3PLs — Legacy Supply Chain and Universal Logistics Holdings Value-Added Services division — had strong years with net revenue growth of 25.7% and 27.4% for $279 million and $423 million, respectively. Legacy has 27 warehouses for 8 million square feet, and Universal manages warehouses with a total of 12.2 million square feet.

Legacy has a mix of customers with concentrations in consumer goods, food and beverage, retail and e-commerce fulfillment and technology.

Universal VAS has a strong automotive and industrial manufacturing support background running sequencing, kitting and subassembly operations for OEMs.

Dedicated Contract Carriage

The asset-heavy dedicated contract carriage (DCC) 3PL segment rounded out the 2021 growth story with more modest growth. Gross revenue increased 15.3% to $23 billion, while net revenue increased 14.7%. Unlike its non-asset DTM brethren, DCC’s growth is limited by each provider’s ability to attract drivers and invest capital in equipment. Those 3PLs with freight brokerages that could handle “overflow” business from DCC operations tended to do well.

Traditional DCC contracts have one- to three-year terms with specific trucking assets being dedicated to customers. This makes DCC contracts much “stickier” than standard shipper-carrier trucking contracts.

In 2020, the Top 25 DCC providers had a total of 68,494 power units. This number only expanded 3.5% in 2021, which is significantly lower than the 14.7% increase in net revenue pointing to substantial year-over-year rate increases for DCC 3PLs.

J.B. Hunt's Dedicated Contract Services fleet boasts 11,689 power units in dedicated. (J.B. Hunt)

The DCC segment leader, J.B. Hunt Dedicated Contract Services (DCS), grew its fleet 16% from 2020 and now boasts 11,689 power units in dedicated. DCS’ above-average net revenue growth of 17.4% to $2.6 billion bested its fleet growth and put its DCC market share just over 11% on a net revenue basis. It has more than 160 customers, and A&A estimates that half of J.B. Hunt’s dedicated tractors are tandem axle sleepers. About as many are day cabs used in regional operations. A significant part of Hunt’s DCS operations involves direct-store delivery. It also has developed a large last-mile delivery network that has significant home-delivery capabilities.

Penske Logistics has grown into the second-largest dedicated fleet with 8,505 power units. Penske’s legacy in DCC goes back to Leaseway, which was a major innovator in transportation and logistics. Leaseway was a founder of DCC in the late 1970s. Penske provides Cardinal Health with more than 400 tractors in DCC. For Wawa stores on the East Coast, it uses 38-foot trailers for deliveries to 575 locations. In July 2018, Penske Logistics acquired dry-van truckload and DCC provider Epes Transport System of Greensboro, N.C., with its more than 1,100 drivers, 1,048 company-owned tractors and 6,065 trailers. At the end of 2020, Penske Logistics acquired major food and perishables specialized DCC provider, Black Horse Carriers, which ranked 13th on A&A’s 2019 Top DCC Providers list with 2,235 power units. Its combined DCC revenues are estimated at over $1.5 billion.

Ryder Supply Chain Solutions, through its Ryder Dedicated Transportation Solutions division, has the third-largest fleet with 5,300 power units. It realized year-over-year net revenue growth of 13.5% to $1.1 billion. Like Penske, Ryder is heavily involved in automotive logistics. It is a lead logistics provider for most GM plants and services Chrysler/Fiat, Toyota and Honda, plus a multitude of tier-one suppliers. In addition to DCC, Ryder runs complementary inbound supply chain management, sequencing centers and just-in-time operations.

Werner Dedicated ended 2021 with slightly above-average net revenue growth of 14.9%, expanding to $1.2 billion. It now ranks fourth with 5,235 power units in DCC and manages more than 120 individual customer fleets ranging from one to over 100 tractors. About 70% of the fleets are managed on-site at customer locations, and approximately 30% of its smaller customer fleets are managed from Werner Enterprises’ operations center in Omaha, Neb. In July 2021, Werner announced the acquisition of an 80% stake in ECM Transport for $142.4 million. ECM Transport based in Cheswick, Pa., provides interregional and dedicated truckload services. In November, Werner purchased Monroe, Conn.-based final-mile logistics services provider NEHDS Logistics for $64 million, with a $4 million earnout.

Evan Armstrong is president of Armstrong Associates Inc. The Transport Topics Top 100 Logistics Companies list is presented in cooperation with Armstrong Associates.

Want more news? Listen to today's daily briefing below or go here for more info: