Diesel Price Drops 4.7¢ to $4.586 a Gallon

[Stay on top of transportation news: Get TTNews in your inbox.]

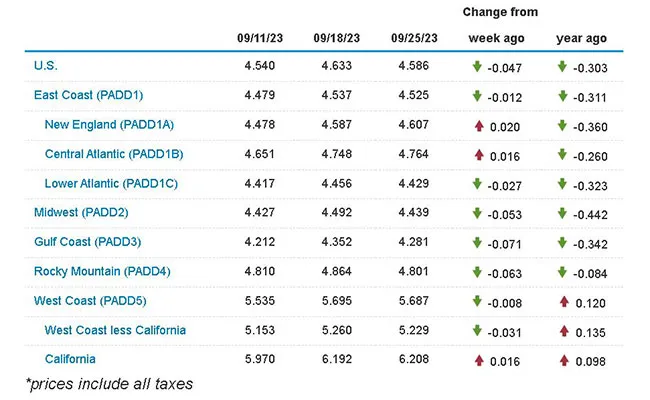

The national average diesel price paused from its recent surge, falling 4.7 cents to settle at $4.586 a gallon, according to Energy Information Administration data released Sept. 25.

The average price of trucking’s main fuel climbed for nine consecutive weeks prior, adding a steep 82.7 cents in total.

On-highway gasoline’s average price also fell, declining 4.1 cents to reach $3.837, as demand is on its seasonal decline following the long Labor Day weekend.

The last time diesel took a downswing was in data released July 3, when it shed 3.4 cents to fall to $3.767 a gallon.

A gallon of diesel now costs 30.3 cents less on average than it did at this time in 2022. In contrast, at the end of June, the discount to 12 months earlier was in excess of $1.90.

Diesel’s average price fell in seven of the 10 regions in EIA’s weekly survey and rose in three. The largest decline of 7.1 cents came along the Gulf Coast. The biggest increase was in New England at 2 cents.

U.S. On-Highway Diesel Fuel Prices

EIA.gov

“The fall price rally has been seasonally attuned,” said David Thompson, an executive vice president at Washington-based brokerage Powerhouse, adding that there was still a little bit of time left for prices to continue to rise. The last week of September tends to be the peak of the shipping season, but there’s an understanding that demand in the agricultural sector has not crested yet.

Trucking companies are playing catch-up after the speedy ascent of diesel prices. When prices rise this fast, it is more difficult for surcharges to keep pace, Leonard’s Express CEO Kenneth Johnson said.

“It is always a challenge to make sure our surcharges are in alignment” with such heady price increases, Johnson told Transport Topics. Farmington, N.Y.-based Leonard’s Express ranks No. 91 on the Transport Topics Top 100 list of the largest for-hire carriers in North America.

Larger carriers like Leonard’s Express are somewhat insulated from diesel prices’ dizzying race higher by the contracts they have in place. Smaller carriers are more exposed.

“It is going to be a really big deal for smaller fleets” because they rely on spot deals and business negotiated through brokerages, Johnson said, adding that he had heard of some smaller carriers staying on the sidelines but not leaving the business while prices settle down.

U.S. average on-highway #diesel fuel price on September 25, 2023 was $4.586/gallon, DOWN 4.7¢/gallon from 9/18/23, DOWN 30.3¢/gallon from year ago #truckers #shippers #fuelprices https://t.co/lPvRNZG7iO pic.twitter.com/0CKkyoGOUJ — EIA (@EIAgov) September 26, 2023

U.S. average price for regular-grade #gasoline on September 25, 2023 was $3.837/gal, DOWN 4.1¢/gallon from 9/18/23, UP 12.6¢/gallon from year ago #gasprices https://t.co/jZphFa0Ptd pic.twitter.com/oIrFkLBDA9 — EIA (@EIAgov) September 26, 2023

Anytime diesel and gasoline prices increase, particularly if it is sharply, inflation rises, which hurts the economy, Johnson said, thus hurting business for the trucking industry.

And in the medium term, bullish factors are still driving the wholesale and therefore retail diesel market, with demand stronger than supply in the U.S., Thompson said. Inventories, as a result, are failing to grow, and therefore prices continue to find support, he added.

The U.S. produced 4.782 million barrels per day of diesel in the week that ended Sept. 15, figures published Sept. 20 by EIA show, which “falls desperately short of combined domestic and offshore demand needs,” Tom Kloza, Oil Price Information Service founder and energy analyst, wrote on X, formerly known as Twitter.

Quick EIA analysis: Today's report could ignite another diesel rally. Domestic demand surges by 588k/day and refiners run 332,000 b/d less crude & feedstock. Output of 4.782-million b/d falls desperately short of combined domestic and offshore demand needs. — Tom Kloza (@TomKloza) September 20, 2023

Supplies of the crude that produces the most diesel are lower than usual too because of extended production cuts by Saudi Arabia and its OPEC+ allies. The price that must be paid for such crude grades is also on the rise, according to EIA.

The typical price relationships that medium sour and heavy sour grades have with sweet crudes has been reversing, EIA said Sept. 25. Most of Saudi Arabia’s crude contains in excess of 1% sulfur, EIA’s threshold for classifying crude as sour, and the output cuts have boosted prices for sour barrels more than sweet.

If the Saudi production cuts continue beyond the end of 2023, further support will be forthcoming for crude prices and therefore diesel prices, analysts say.

Investment bank JPMorgan Chase & Co. expects a 1.1 million-barrels-per-day global crude supply-demand gap in 2025, which it forecasts will widen to 7.1 million barrels per day in 2030, driven by both a robust demand outlook and limited supply sources. The bank expects demand to increase by 5.5 million barrels per day in 2030 compared with 2023.

As a result, “we do not find oil prices in the $100-a-barrel to $120-a-barrel range to be ‘demand destructive,’ as they are broadly in line with historical prices when measured in real terms and assuming higher for longer interest rates,” a team led by Christyan Malek wrote in a Sept. 22 research note.

Benchmark front-month WTI crude was trading around $90 a barrel Sept. 26 after trading below $70 a barrel at the end of the second quarter of 2023.

If the supply-demand imbalance worsens, the JPMorgan analysts wrote in the note, then crude prices of $150 are not out of the question by 2026.

Want more news? Listen to today's daily briefing below or go here for more info: