Truck Stocks Plunge in 2015

Trucking companies’ shares, which declined faster last year than other transport stocks and the broader financial markets, are likely to keep falling in early 2016. The underlying reason: a sharp shift in freight capacity, industry analysts believe.

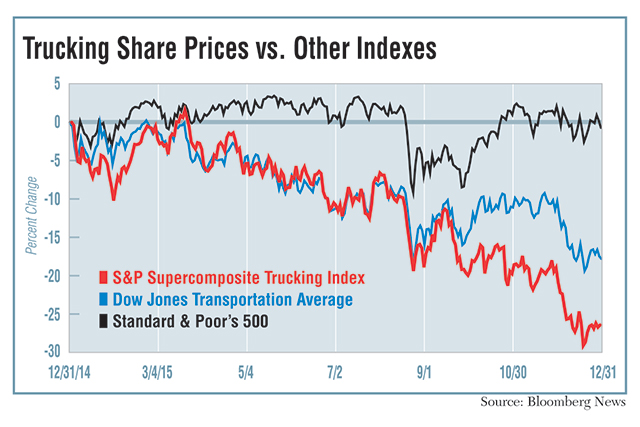

The 27% drop during 2015 in the Standard & Poor’s index of trucking stocks, which includes such household names as Swift Transportation and Werner Enterprises, exceeded the 18% decline in the Dow Jones Transportation average, which also includes railroads and airlines. Swift and Werner rank Nos. 6 and 16, respectively, on the Transport Topics Top 100 list of the largest U.S. and Canadian for-hire carriers.

Meanwhile, the S&P 500 ended the year almost exactly where it began, dropping 0.7%.

On an individual basis, Expeditors International of Washington was the only company, out of the 30 freight companies’ shares tracked by TT, that rose on a year-over-year basis, increasing 3%. Meanwhile, Saia Inc.’s shares declined the most at 59%. Expeditors ranks No. 5 on the Transport Topics Top 50 list of the largest logistics companies in North America, and Saia is No. 29 on the for-hire TT100.

By sector, the largest drop was 39% among less-than-truckload carriers, which included a 56% decline at No. 17 Roadrunner Transportation Systems. Truckload shares fell 30% on average, with declines of more than 50% at Swift, No. 42 Celadon Group and No. 67 P.A.M. Transportation. Package carriers were hurt less, with a 16% decline at No. 2 FedEx and 12% at No. 1 UPS. Logistics shares on average dropped 19%, including 33% at XPO Logistics, ranked No. 12 on the TT Logistics 50.

Keybanc Capital Markets analyst Todd Fowler summarized the reasons for the 2015 tumble.

“Expectations were high entering the year following the tight capacity environment experienced in 2014,” he told TT on Jan. 6. “Incremental capacity entered the market as carriers increased driver pay and purchased more trucks. Freight activity slowed, reflecting weaker industrial and manufacturing end-markets, as well as elevated inventories throughout the supply chain.”

BB&T Capital Markets analyst Thom Albrecht pinpointed the impact on capacity from both inside and outside the trucking industry.

In terms of freight demand from the economy as a whole, trucking was hurt by the swing of 5 percentage points in industrial production, from 4% growth in 2014 to a 1% drop in 2015, he told TT last week.

At the same time, the supply of trucking capacity expanded in two ways, he explained. Fleets grew about 5% larger by purchasing new equipment and paying drivers more to keep them in the seats of that new equipment. In addition, fleets also had 2% or 3% more capacity because they would use trucks more efficiently after hours-of-service restart rules were relaxed late in 2014.

As 2016 dawns, the same forces are affecting the market.

“Many investors have extrapolated the weak freight environment, particularly in the second half of 2015 [into 2016],” John Larkin, a Stifel Nicolaus analyst told TT last week, saying that share prices could languish in the first quarter.

Analysts cited several factors that could impact fleets’ shares later this year.

Albrecht said he believes freight shares could be buoyed by mid-year, at least modestly, by trimming excess capacity to bring supply and demand back into balance in conjunction with stabilization of industrial production.

Factors such as reductions in inventory, increased exports and higher energy prices that encourage exploration could resuscitate the 2016 trucking economy and share prices, Larkin said. Shares also could rise if fleets’ earnings exceed investor expectations that have been reduced by events in 2015, he added.

“Investors are looking for more certainty with respect to the overall economy and firming capacity before seeing a sustained increase in shares,” Fowler said.

However, he also said today’s “relatively cheap” shares could tempt investors, starting in the second half of 2016, as long as factors such as lower capital spending and equipment purchases control capacity.

Kevin Sterling, another BB&T Capital Markets analyst, said 2016 could be a tough year for UPS, FedEx and Expeditors because of their exposure to international markets that appear to be weakening, such as China.

Sterling said the first half of 2016 will be difficult for investors, though he said the fast growing e-commerce business could be helpful in turning around very cyclical transport shares if there is a pickup in the economy.

Cowen & Co. analyst Jason Seidl stressed that shares could look better later in 2016, due to the easier comparisons to last year’s second half, when the S&P trucking index lost 16 of its 27 percentage point decline.

Benjamin Hartford at Robert W. Baird & Co. noted that the freight transports’ share of price trends have trailed the broader stock market for far longer.

The underperformance actually began in 2011, he said, when the Institute for Supply Management’s factory index reached a peak in the current economic cycle, sparking freight demand growth.

Hartford said “our 2016 freight demand outlook is cautious” due to current economic conditions.

“We are optimistic about the longer-term [share price] dynamics” as capacity tightens in 2017 and beyond due to regulatory, demographic and consolidation trends, he added.