Business-Spending Slowdown Casts Shadow on Solid GDP Report

Consumers drove the U.S. economy to better-than-expected growth in the third quarter, but a steep slowdown in business spending raised concerns about whether the strength in the expansion is sustainable.

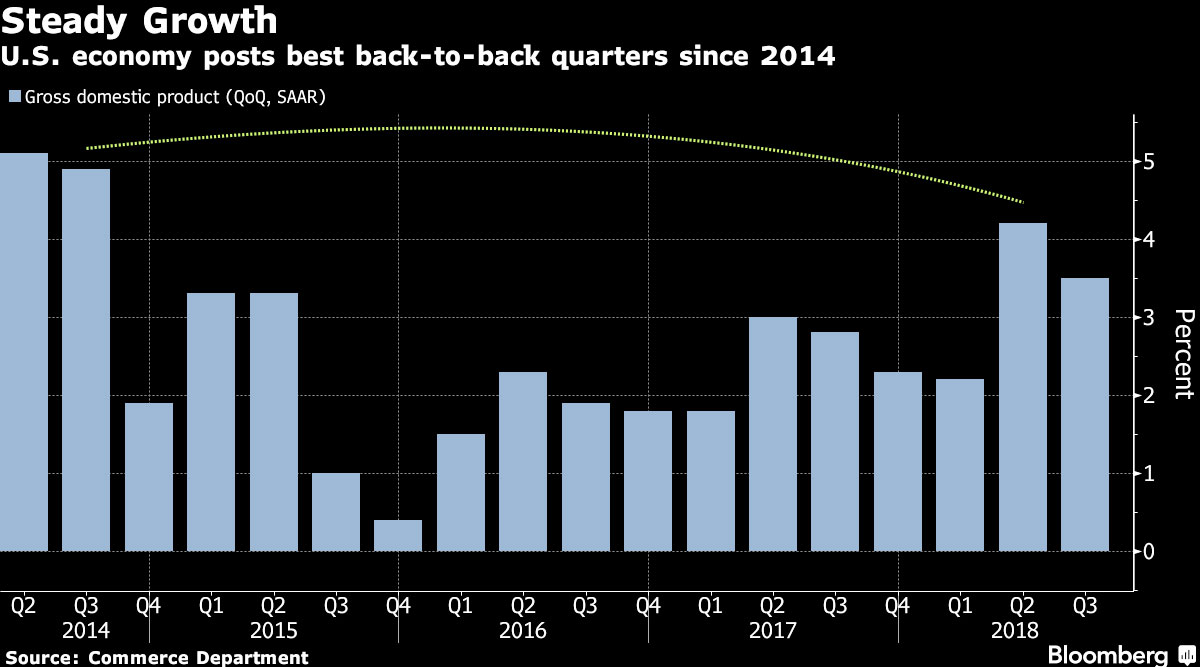

The 3.5% annualized gain in gross domestic product, following 4.2%, marked the best back-to-back quarters since 2014, according to the Oct. 26 Commerce Department report. The rise in consumer spending, which accounts for about 70% of the economy, unexpectedly accelerated to an almost four-year high of 4%.

Yet amid President Donald Trump’s trade war, nonresidential business investment rose at a 0.8% pace, the weakest since 2016 and down from 8.7% in the prior quarter. Companies paused spending earlier than some economists expected given the fiscal boost from Republican-backed tax cuts.

While a solid labor market and gradually rising wages are buoying consumers, investors took little comfort from GDP: The S&P 500 stock index plummeted on Oct. 26, entering a correction following reports showing the growth engines of Amazon.com Inc. and Alphabet Inc. sputtered last quarter. Analysts said the Federal Reserve probably remains on track for a December interest-rate increase, its fourth of 2018, though the GDP details suggest the economy isn’t shifting into a permanently higher gear.

“The fate of the consumer rests with the willingness and ability of businesses to keep hiring,” said Julia Coronado, president of MacroPolicy Perspectives LLC and a former Fed researcher.

The slowdown in business spending “came earlier and was more than we expected, given where the stimulus is,” Coronado said. “That suggests some of this stimulus won’t last, it’s not going to turn into higher-trend growth through the channel of investment and greater capacity and greater potential growth.”

Trade Drag

Trade also dragged down growth by the most in 33 years, amid ongoing tariff battles with large trade partners such as China. Together with the business-spending figures, they’re an early indication that firms might be cooling on the kinds of activities that drive expansion, employment and wages.

A core measure that economists monitor for a better sense of underlying demand — final sales to domestic purchasers — increased at a 3.1% pace, slowing from 4%. It excludes the more volatile trade and inventories components of GDP.

Fed officials have recently talked about “optimism and acceleration in capital spending and could it lift the supply side,” but the slowing in business investment “is inconsistent with a sizable improvement in spending,” said Michael Gapen, chief U.S. economist at Barclays Plc and a former official at the central bank.

“In the big picture, what we’re trying to ascertain is: Is fiscal stimulus transitory or will it help sustain economic growth longer term? This report shows the fiscal stimulus has a transitory response.”

More broadly, the International Monetary Fund earlier this month cut its global growth forecast for the first time in two years, blaming escalating trade tensions and stresses in emerging markets. World GDP would fall further should Trump follow through on all his trade threats, including global duties on cars, the IMF said.

On the other hand, the Trump administration is optimistic, particularly as the report showed inflation remains contained: Excluding food and energy, the Fed’s preferred price index also rose at a 1.6% rate. Trump has criticized the Fed for raising interest rates without signs of significant inflation.

“We really do feel like we’re in that Goldilocks moment where we’re getting good GDP growth but we don’t have the inflation that you traditionally might have seen with this type of market,” Mick Mulvaney, director of the Office of Management and Budget, said on Bloomberg Television.

Roberto Perli, a partner at Cornerstone Macro LLC in Washington and a former Fed economist, said the GDP report is consistent with the central bank’s forecast. “The Fed outlook is basically validated by the data,” he said. “There’s no incentive to change policy direction.”

Housing remained a weak spot in the economy, posing the third consecutive drag on GDP growth, with a contraction of 4%. Recent reports indicate the industry is slowing amid higher prices and rising mortgage rates, as well as a lack of affordable listings.

That’s an indication that consumers are also feeling the bite from rising interest rates, according to Gapen of Barclays.